Freelance culture is thriving in every part of the world, and more people are freelancing as their main source of income. According to recent data, there are more than 1.57 billion freelancers worldwide and the average freelancer earns anywhere from $20 to $70 per hour depending on the job.

While freelancing enables you to have flexible working hours, there’s always the possibility of your income becoming irregular, especially if some of your clients stop using your services, they don’t pay on time, or you have unreliable workloads.

Having lean months is one of the downsides of freelancing, and freelancers that are aware of this fact understand that being adept at income management and keeping track of expenses is crucial to avoid debt. Moreover, it’s a good way to ensure that you always have funds whenever you need them.

In this article, we share five tips from experienced freelancers on how to manage your finances as a freelance proofreader.

Tip 1: List Your Monthly Expenses

Understanding how you spend your money is the key to making sure that you’re financially healthy. If you don’t know where to start, it’s time to sit down and figure out where your money goes.

List all your home office expenses like your printer, computer, and other office supplies you use for your freelance proofreading jobs. Next, list all your living expenses, like rent, utilities, food, transportation, health expenses, credit card payments, and other necessities.

Beside each category, write down the amount that you need to pay every month. Keep in mind that this does not include your personal savings, emergency expenses, or leisure and entertainment expenses.

Add everything up. The total is roughly the amount that you need to make every month. Make sure that your hourly rates are high enough to reflect your time, effort, and experience levels. If you’re making enough money through proofreading to cover everything, then you’ve probably got a pretty solid gig and an accurate hourly rate. If not, you may have to look into getting more online proofreading jobs, increasing your rates, or a second source of income.

Pro tip: Don’t forget to always pay your bills on time, and don’t spend more than what you have to on items that don’t have a fixed amount, such as groceries.

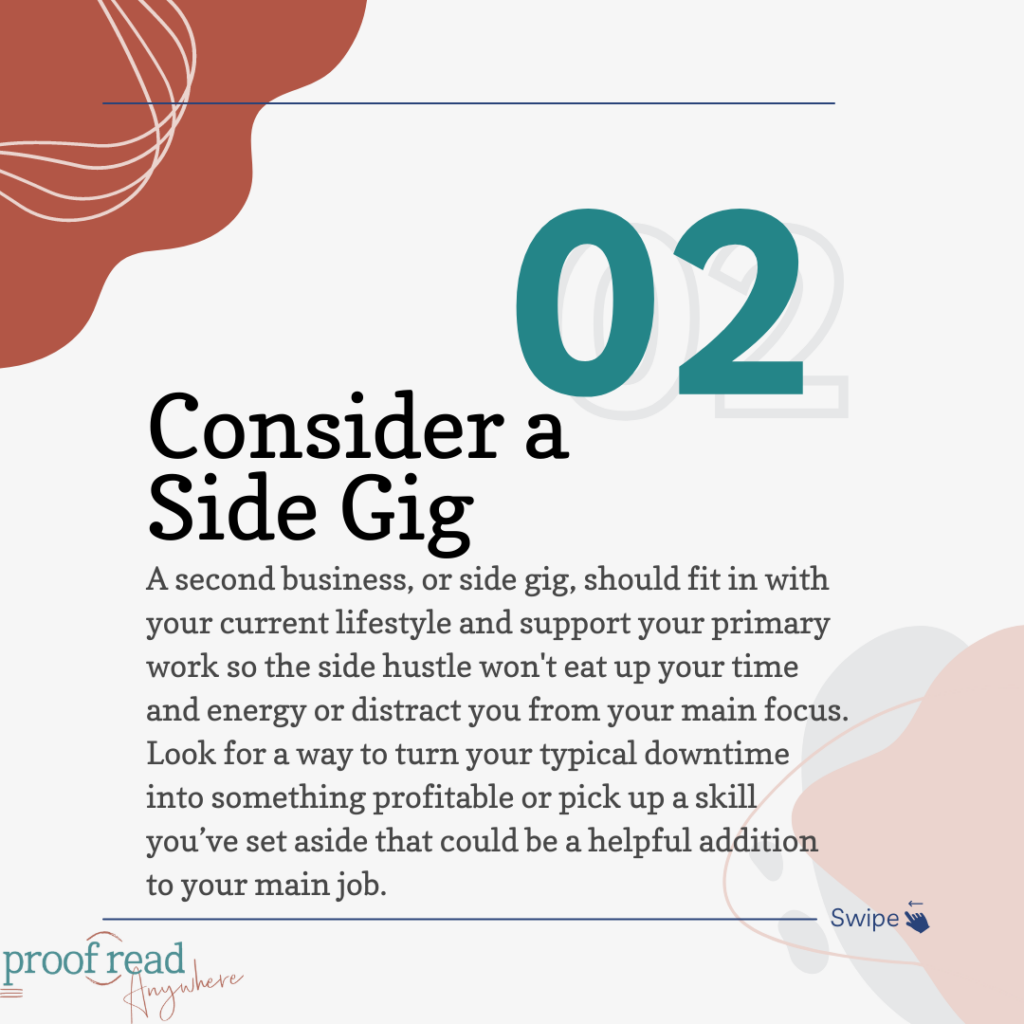

Tip 2: Think About Starting a Side-Gig

Finding potential clients can be difficult, but with the rise of online proofreading jobs, it’s becoming easier to find more work. Getting additional proofreading jobs is always an option if you want to earn more than what you’re currently getting, but if you want to try a different way to earn money, think about starting a second business.

A second business, or side gig, should fit in with your current lifestyle and support your primary work so the side hustle won’t eat up your time and energy or distract you from your main focus. Look for a way to turn your typical downtime into something profitable or pick up a skill you’ve set aside that could be a helpful addition to your main job.

For instance, if you regularly take walks during the day as a way to get breaks from work, consider starting a dog walking business. Not only do you get to exercise, but you also get to earn some money while you’re out and about — both of which are beneficial to your primary business.

Some of the best business ideas have been rejected by investors, yet the businesses have gone on to achieve incredible success once customers saw their potential. For example, if you’ve got an idea for a new product or you’ve developed software or an app, consider selling it online. Start by posting your creation on Etsy, market your business and connect with clients on social media, and build a website as the home for your business.

Don’t be afraid to put your skills out on the market. Many side gigs can become lucrative businesses and support your primary freelance proofreading business.

Tip 3: Schedule Your Invoices

Scheduling your invoices helps you track multiple payments from multiple clients and ensure you get paid on time. For instance, professional proofreaders can bill different clients on different schedules to stretch their money and eliminate lean months. You might bill one client on a weekly basis, while another client gets billed every 15 days. Additionally, consider letting your proofreading clients know that they may incur extra costs for late payments.

Tip 4: Save Up for a Rainy Day

Experienced proofreaders should always make a point of saving money in case there are extra slow months or emergencies. For your personal finances, your savings account should have enough money to sustain you for six months in case you get sick, clients suddenly end their contracts with you, or there is a reduction in the flow of projects.

To make sure that some of your earnings go into the bank and aren’t spent, set up an automated savings account. If you get paid through PayPal, consider opening a PayPal savings account — which acts like a typical bank account with interest to help you meet your financial goals.

If you have a separate budget for your professional proofreading business, make sure to invest profits back into the business, while still paying yourself a decent salary that leaves plenty of room for personal savings.

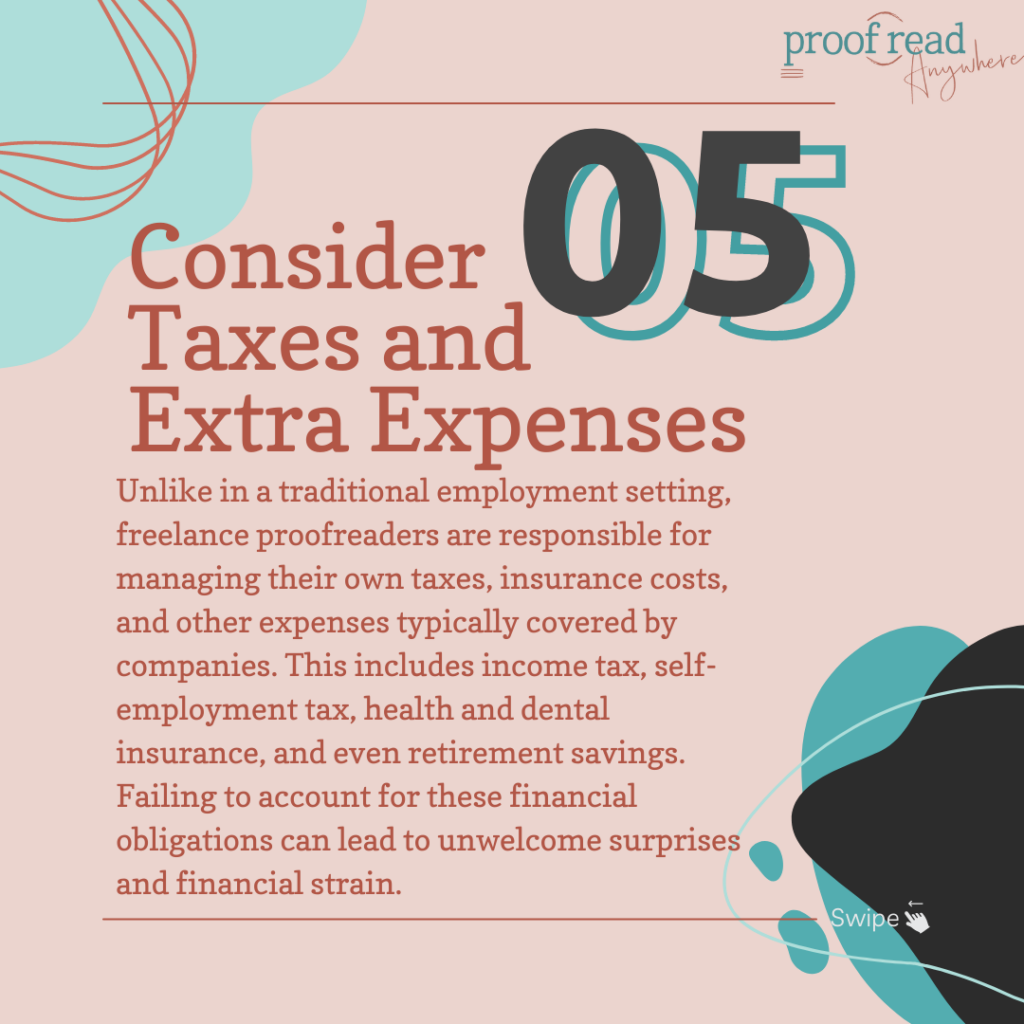

Tip 5: Consider Taxes and Extra Expenses

In the world of freelance proofreading, you can enjoy the freedom and flexibility that come with being your own boss. However, it’s essential to account for the additional responsibilities that go along with freelancing.

Unlike in a traditional employment setting, freelance proofreaders are responsible for managing their own taxes, insurance costs, and other expenses typically covered by companies. This includes income tax, self-employment tax, health and dental insurance, and even retirement savings. Failing to account for these financial obligations can lead to unwelcome surprises and financial strain.

Freelancers should always put aside extra money, or a certain percentage of income, each month to cover these costs. To pay taxes and plan for extra expenses, the U.S. Small Business Administration has so many amazing resources.

Our Thoughts

In order to maintain a successful and sustainable professional proofreading career, it’s crucial to budget for expenses and make informed decisions about how to allocate income and plan for the future. Consider these tips for managing your finances so you can stay within your budget, increase your savings, and continue to have a flexible work routine while achieving your financial goals.

By staying on top of your responsibilities and planning ahead, you’ll surely reap the rewards of your hard work and independence.

This is a great article with very useful information. Your article is probably the best I read today.

I regret to say the thumbnail has a spelling error – Mange vs Manage 🙂